Unless you are new to investing, you have probably heard of an IRA, which stands for an individual retirement account. An IRA is simply a financial account set up by a financial institution that allows an individual to save for retirement with tax-free growth on a tax-deferred basis.

Why Invest In An IRA

Financial experts suggest that you will need income up to 85% of your pre-retirement income in order to retire comfortably. The total amount of money you will need to have saved depends on your annual income. However, the general retirement savings that most financial advisors suggest is $1 million; however, I believe that number can be reduced to $200,000 if you retire abroad by relocating to a less expensive country. Nonetheless, savings $200,000 may be hard to do if you put your monthly savings into a typical checking or savings account that pays little or no interest.

In order for your money to grow exponentially, you need compound interest working for you. This is where investing in something like an employer-sponsored 401(k) (which is now 40 years old) can help you. A 401(k) allows you to contribute pre-tax income into a retirement account where the earnings provided by compound interest grow tax-free. Unfortunately, once you start withdrawing your 401(k) savings you have to pay taxes on the amount you withdraw.

If your employer does not offer a 401(k) plan for you to invest, I strongly encourage you to invest in an IRA. Even if your employer does have a 401(k) plan, the matching contributions might not be enough to accumulate the savings you need. Fortunately, you can contribute to both a 401(k) and an IRA.

There are two types of IRAs and each has different advantages.

Traditional IRA

A Traditional IRA allows you to make contributions with money you can potentially deduct from your federal and state tax return during the year you make the contribution. Any earnings from a Traditional IRA can potentially grow tax-deferred until you withdraw them at retirement. Withdrawals in retirement are taxed at ordinary income tax rates.

Age and Income Restrictions

Anyone with earned income who is younger than 70 1/2 can contribute to a Traditional IRA. Whether the contribution is tax deductible depends on your income and whether you or your spouse are covered by a retirement plan through your job, such as the 401(k) mentioned above.

The main advantage the Traditional IRA offers is that, in general, you avoid taxes when you put the money in.

Required Minimum Distributions

The main disadvantage of a Traditional IRA is the withdrawal rules. You are required to start taking required minimum distributions (RMDs) – mandatory, taxable withdrawals of a certain percentage of your funds at age 70 1/2, whether you need the money or not. To begin taking penalty-free, “qualified” distributions, owners must wait until they are age 59 1/2.

Estate Planning

Generally, you must take distributions during your lifetime or within five years after the original account holder has passed away. With an inherited Traditional IRA, heirs will pay taxes on any distributions taken.

Roth IRA

A Roth IRA allows you to make contributions with money you have already paid taxes on (after-tax), and your money (just like the Traditional IRA) can potentially grow tax-free, with tax-free withdrawals in retirement, provided that certain conditions are met.

Age and Income Restrictions

Unlike Traditional IRAs, the Roth IRA does not have age restrictions, but they do have income-eligibility restrictions. Starting in 2019, single tax filers must have a modified adjusted gross income of less than $137,000 to contribute to a Roth IRA (contribution limits are phased out starting with a modified AGI of $122,000.) Married couples filing jointly must have modified AGI of less than $203,000 in order to contribute to a Roth; contribution limits are phased out starting at $193,000.

Required Minimum Distributions

Roth IRAs do not require any withdrawals during the owner’s lifetime. There are no required minimum distributions. If you have enough other income, perhaps by passive income sources, you can let your Roth IRA continue to grow tax-free throughout your lifetime. This will ensure that you never run out of money. Roth contributions (but not earnings) can be withdrawn penalty- and tax-free at any time, even before age 59 1/2. If you are under age 59 1/2, you can withdraw up to $10,000 of Roth earnings penalty-free to pay for qualified first-time home-buyer expenses, provided at least five tax years have passed since your initial contribution.

Estate Planning

The Roth IRA is also an ideal wealth-transfer vehicle. One of the greatest benefits of a Roth IRA, especially over other retirement accounts such as the 401(k) and Traditional IRA retirement plans, is that a Roth IRA can be passed on to an heir when you die.

Beneficiaries of Roth IRAs do not owe income tax on withdrawals and can stretch out distributions over many years. However, Uncle Sam may still get money through estate taxes, but with some planning you can avoid this.

Investing in a Roth IRA keeps the government from taxing our investment and it is ideal for estate planning. The investment can be passed down to your heirs allowing you to leave a legacy. Your beneficiaries can receive the funds, just as you would have in retirement, tax-free!

You are allowed to withdrawal Roth IRA earnings penalty-free after age 59 1/2. However, Roth IRAs require that the first contribution is made at least five years before the first withdrawal, in order to avoid incurring a tax payment.

Rollover IRA

The third type of IRA is the Rollover IRA. A Rollover IRA allows you to contribute money “rolled over” from a qualified retirement plan into a Traditional IRA account. Rollovers involve moving eligible assets from an employer-sponsored plan, such as a 401(k) or 403(b), into an IRA.

How Much Should You Contribute

You should try to contribute the maximum amount to your IRA each year. The sooner you start investing the better. This will allow you to get the most out of your savings. Fidelity offers a free IRA Contribution Calculator to help you determine how much you can contribute.

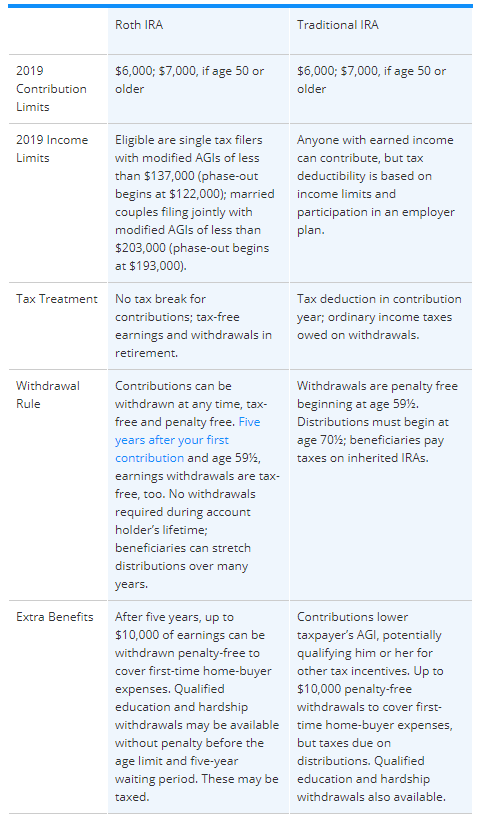

Comparing Traditional IRAs to Roth IRAs

This table lays out the differences between the two types of IRAs. It’s important to keep in mind that Congress can change the rules governing these accounts at any time. The regulations may be very different when you retire.